Inflation Nation: You Should be "Fed" Up by Now

Inflation Nation: You Should be "Fed" Up by Now

Runaway inflation seems to be on the horizon, but how did we get to this point?

The Federal Reserve is a crucial part of our nation’s economic stability. Since 1913, when the institution came into existence via the Federal Reserve Act, the “Fed” has operated as the central bank of the United States. A central bank is a financial institution given priority and often total control over the production and distribution of money and credit for an entire nation. In modern economies, central banks, like the Fed, are usually responsible for the formulation of monetary policy and the regulation of member banks.

The key privilege that central banks operate under is that of “legal monopoly” - essentially, central banks truly hold a monopoly in the industry, but do so under the legality of a government mandate.

As the central bank of the most powerful country in the world, the Fed is arguably the most powerful financial institution in the world. Since its inception, the Fed has largely operated under mysterious circumstances. Its monetary policies and decisions severely impact the United States’ economy, however, rationale for such policies and decisions are rarely, if ever, made truly available to the public.

Ask any tin-foil-hat-wearing, speculative citizen, and you’ll get the same sentiment. Most people do not like the Fed. They likely won’t be able to put their finger on why, exactly. The answer probably comes down to one broad issue: control. The Fed is the sole wielder of economic power and control, operating independently of the three branches of Government in the United States.

The Fed was initially created as a means to provide the country with a safe, flexible, and stable monetary and financial system. In practice, however, it seems the Fed’s policies have led to anything other than a “stable” financial system; recessions and economic downturns have cyclically plagued the American economy since 1929.

The Fed’s control is not only theoretic, it’s geographic as well - the Fed is composed of 12 regional Federal Reserve Banks that are each responsible for a specific geographic area of the U.S. Through a blanket approach that engulfs every corner of the contiguous U.S., the Fed can exercise total control when enacting policy.

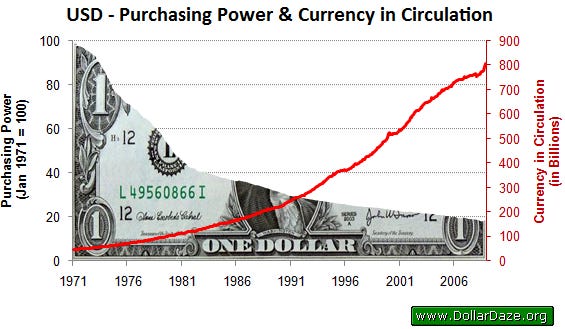

The Fed’s chief purpose is to ensure financial stability for the entire U.S., wielding tools like printing money and raising interest rates to do so. In fact, it’s likely that you’ve only really heard the Fed mentioned in conversations dealing with inflation. Yes, inflation, otherwise known as a hidden tax on American citizens. From a more economic point of view, inflation is the decline of purchasing power of a given currency over time. Inflation in practice is seen through systematic price increases that outweigh any corresponding increase of wages. As inflation rises, individuals are able to buy fewer and fewer goods with the same amount of money.

So what causes inflation? Well, the consensus view among economists is that sustained inflation occurs when a nation’s money supply growth outpaces economic growth. In layman’s terms, inflation occurs when a nation prints money at a rate that exceeds the nation’s rate of economic growth. Why is this? Well, if the rate of money in circulation outpaces the corresponding level of economic growth, this means there are more dollars available to buy fewer goods. When analyzed in light of the definition stated above, this would result in a consumer being able to purchase fewer goods with a certain amount of dollars.

Inflation is a tricky nut to crack. If you ignore it, it can decimate an economy by dwindling consumers’ purchasing power. There are multiple methods by which inflation can be dealt with, and all methods are routinely employed by the Fed in times of economic crisis. The most popular method to combat inflation is raising interest rates. From a purely economic point of view, the raising of interest rates should, in theory, encourage consumers to spend less money. When considering the definition of inflation, such a policy would theoretically result in fewer dollars being circulated and thus easing the burden of inflation.

Inflation isn’t always a bad thing, though. The Fed expects an annual inflation rate of 2%, and a problem arises only when inflation exceeds 2%. I’m not sure if you’ve watched the news recently, but inflation is currently sitting at 8.6%. How could such a startling figure be true? Well, there are likely two main causes for such runaway inflation, and we’ll discuss them below. They can both be traced back to direct policies put in place by the Fed within the last two years.

As previously stated, the Fed holds sole control over the financial policies instituted by American banks. One of the principal purposes of the Fed, since its inception in 1913, has been to set reserve ratio requirements. What are these? Well, prior to 1913, there was no set requirement for how much physical currency banks must hold in their vaults. Essentially, this meant that banks could loan out as many dollars as they desired. A problem arose when consumers felt uncertain of banks’ stability, and in times of severe economic instability, a “run on banks” would occur. This meant that consumers would withdraw all money from their bank accounts in droves. Such an occurrence routinely led to banks declaring bankruptcy due to not having enough money to pay out the full balance of every account-holder looking to close their account. To combat this, the Federal Reserve was created in 1913. Shortly after the Fed’s creation, reserve requirements for three different types of banks were set at 13%, 10%, and 7%, respectively.

Since that time, most banks have operated at a 10% reserve ratio. This means, if a bank has $10,000,000 in currency on its books, it is only required to have $1,000,000 cash in its vault at any given time. The system seems hilariously foolish - a severe financial panic would surely result in an extreme run on banks. Bear with me and you’ll learn that the situation has only gotten worse in recent years.

On March 26, 2020, the Federal Reserve Board announced that the reserve requirement ratios would be set to 0%. That’s right, zero. Since 2020, American banks have not been required to maintain any physical cash on hand. The reasoning for such a drastic decision likely falls on the immense economic hardships experienced as a result of COVID-19.

Regardless of the rationale, this decision poses innumerable risks to our nation’s economy. Effectively, all of the U.S. dollars in circulation are nothing more than play money. Banks are not required to have any physical cash in their vaults, and any run on banks would pose cataclysmic implications unlike anything experienced in our nation’s history.

The Fed’s history surrounding its inception is largely shrouded in mystery. However, one of the principal purposes in creating the United States’ central bank was to mandate reserve ratios across all U.S. banks. The aim was to standardize the amount of dollars each bank must keep on hand, in order to prevent certain banks from going under in the unfortunate scenario of a run on banks. However, such a point seems moot when banks are no longer required to have any cash on hand. This move cannot be characterized as “pulling the rug” out from underneath American consumers, it’s better described as pulling the drain plug out of a bath. There can only be one result.

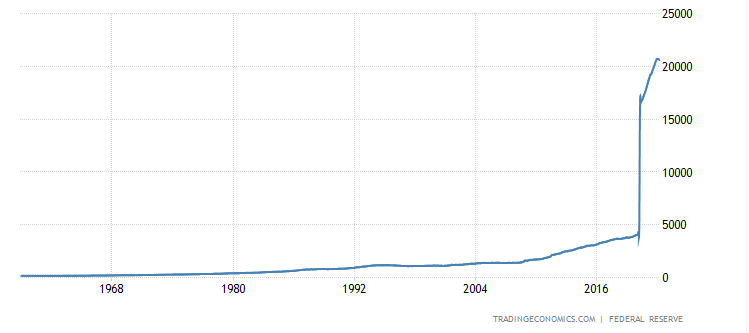

Now let’s examine the Fed’s money-printing policy decisions since 2020. As stated, inflation occurs when the rate of money being put into circulation outpaces the rate of economic growth. For a good idea of our nation’s money supply, look to the M1 money supply. This is a metric employed by the Fed to examine how much money is currently in circulation. The M1 money supply is composed of Federal Reserve notes - a.k.a. bills or paper money - and coins that are in circulation outside of the Federal Reserve Banks and the vaults of depository institutions (a.k.a. banks). Paper money is the most significant component of a nation’s money supply, from an economic standpoint, so the M1 money supply gives a solid depiction of the nation’s economic wellbeing.

Here’s a graph depicting the amount of USD in circulation over the years.

You’ll notice a dramatic spike after 2016. This spike can be attributed to the vast amount of dollars printed and circulated in response to the COVID-19 pandemic. As you can very well see, the money supply effectively quadrupled virtually overnight in 2020. You can blame policy decisions like COVID stimulus packages for that. Surely, the nation was in financial disarray around that time and such a move was warranted. However, if you’re looking for why inflation is currently hovering around 8.6%, the unbridled printing of money is certainly the main culprit. Going even further, when you consider the fact that most of the U.S.’s economic output has dwindled since 2020, the unchecked printing of money seems even more nefarious.

Last but not least, the M1 money supply calculation was recently changed by the Fed in an unprecedented way. Considering the M1 money supply looks at the quantity of dollars in circulation, it stands to reason why dollars in savings accounts would be excluded. Most consumers put dollars into savings accounts for that exact purpose - to save. Such dollars cannot be said to be in circulation. Further, when examining other indicators of inflation, like the Consumer Price Index, most consumers are not tapping into savings accounts to pay for everyday goods.

However, on April 24, 2020, everything changed. Prior to that date, savings accounts were not part of M1. As of April 24, 2020, M1 now includes dollars in savings accounts. This means that the core tenant of how the M1 money supply is calculated was stripped away virtually without warning or explanation. The result is a “cooked book,” or in other words, an inaccurate depiction of the true supply of money in circulation. Such a move will likely have serious financial consequences. Considering the direct relationship that the printing of money has on inflation, it stands to reason that the true figure of inflation far exceeds the number we currently have. How could it not be, considering the unprecedented change of adding savings accounts to the M1 money supply?

The short version of this entire discussion can be stated as follows: in response to COVID-19, the Fed decided to print and circulate vast quantities of money. Considering the decimating effects that the pandemic had on domestic output and economic growth, the unbridled printing of money is certain to result in inflation. When considering the changes made to how the M1 money supply is calculated, the true rate of inflation likely exceeds the figures we are given now. What this means for American consumers is a stripping away of purchasing power unlike anything seen before. Finally, when combined with the Fed’s 2020 decision to end reserve ratio requirements, these financial metrics indicate a tumultuous economic future.

What happens in the case of a recession, when individuals feel their money is no longer safe in American banks? They’ll likely run to banks to withdraw their accounts. In such a scenario, banks, under the Fed’s current economic policies, will likely not have enough physical currency to meet their customers’ withdrawal requests. A complete dissolution and demise of the nation’s financial institutions would likely follow.

Inflation has been historically described as an “invisible tax on the American people,” because it is only the consumer who bears the burden of this hidden beast. Companies can withstand inflation, as all price increases are passed onto consumers in the form of price hikes. Your savings accounts, checking accounts, and other forms of capital will be gutted - the cost of goods will increase at a rate far outpacing any wage increases you’ll receive as a defensive measure.

All of the decisions and policies implemented should be indicate one crucial point: the financial elites sitting comfortably atop the American economy do not care, in the slightest bit, about American consumers. They will shield corporations and fellow depository institutions from economic downturns, while placing the brunt of burden on the shoulders of the American people. This has been the case since the Fed’s creation in 1913, and judging from the policy decisions made during the COVID-19 pandemic, such sentiments seem alive and well to this day. What else could be the rationale for stripping reserve ratio requirements? A decision that could burden only American consumers? Banks will always be bailed out, as history has shown. Who will bail you out when you decide to withdraw your money from a bank, only to learn they don’t have the cash to handle your request?

The Fed should always be viewed under a microscope, and all of its decisions should be heavily scrutinized. Unless some or all of these policies are ended, the financial future of the United States is anything but stable. Considering the Fed’s ultimate purpose - to stabilize the American economy - one can only wonder:

What is going on? What will the future hold?

Interesting, also frightening article. I am one of those people (mostly women I suspect) who suffers from brain freeze when the subject is money. I doubt if I have enough in the bank worth stealing, but I am planning to switch from my (small) bank to a savings bank, especially if I could find one on-line that actually pays interest on savings. I'm kind of hoping for a bank crash, assuming that will put a serious dent in U.S. power, but my brain isn't frozen enough not to realize that those with the least are the ones who'd suffer the most. But this government - if you can call it that - has to go! They don't even bother to pretend anymore that they aren't wholly, completely corrupt.

Hey gotta start somewhere - no shame in that! Kudos for snagging a deal when you can.

I think we have until at least 2023 before it happens. That’s not to say we won’t see food shortages in the fall. I think that’s coming too. Either way, it seems the American people are in for a great degree of turmoil over the next year.

I think as long as you’re in a good spot prior to March of 2023, you’ll be able to weather the storm.